How To Use Post Office RD Calculator?

If you are someone thinking to invest in Recurring Deposits (RD) per month then you should use moneycontain free post office RD Calculator to calculate your maturity amount you would get in future.

It is very important for an investor to know the expected amount in advance and before making the investment. This will ensure whether the selected investment option will serve the financial goal of the investor at the maturity or not. Once an investor has the financial goal in his mind, he can also decide on which investment option to select.

Using this post office RD calculator will help you to be well aware of your financial goals, moreover it helps you in knowing the expected amount you will get after making monthly Recurring deposits for X no. of months or year.

To use the PORD calculator you just need to enter the regular monthly deposits, enter the investment period (in months) and select the expected rate of interest.

That’s it, the RD calculator will show you the future value of your investment with interest earned and total investment made by you in microseconds.

However, before you proceed keep below things in mind:

- The Minimum Amount for opening of account and maximum balance that can be retained for post office RD is Minimum INR 100/- per month or any amount in multiples of INR 10/ with No maximum limit.

- From 01 April 2024, post office RD interest rates are 6.7 % per annum (quarterly compounded).

- The minimum tenure is 5 years (60 monthly deposits) from the date of opening. Although, account can be extended for further 5 years by giving application at concerned Post Office.

- Keep in mind, Interest rate applicable during extension will be the interest rate at which account was originally opened.

So, go ahead and check your monthly post office RD return easily using below PORD Calculator.

How Post Office RD Works?

For more than 150 years, the Department of Posts (DoP) has been the backbone of the country’s communication and has played a crucial role in the country’s social economic development.

It touches the lives of Indian citizens in many ways: delivering mails, accepting deposits under Small Savings Schemes, providing life insurance cover under Postal Life Insurance (PLI) and Rural Postal Life Insurance (RPLI) and providing retail services like bill collection, sale of forms, etc.

The DoP also acts as an agent for Government of India in discharging other services for citizens such as Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS) wage disbursement and old age pension payments.

Established in 1854, With more than 1,55,000 post offices, the DoP has the most widely distributed postal network in the world.

One of the key reasons behind the success of post offices in India is the range of products and services they offer. One such popular offering is Recurring Deposit, known as National Savings Recurring Deposit Account.

In simple terms Recurring Deposit or famously known as RD is a type of fixed term deposit on a monthly basis in your Recurring Deposit account opened by post office.

When you are saving a fixed amount of money every month through RD, post office compounded interest rate on quarterly basis, which makes your investment grow over a period of time.

Once the maturity period of your RD is over you would receive the lump sum amount with interest. This type of financial instruments gives you peace of mind as the returns are already fixed and does not fluctuate with any adverse market movements.

Moreover with the flexibility of every month deposit it makes a good habit of saving some money for your future as well. If we talk about other form of investments such as Monthly SIP in an mutual fund, the returns are not guaranteed, It may give you higher or lower return than your expectation.

That is why usually people prefer to invest in post office RD more compare to any other form of investment. Post Office Recurring deposits are made for fixed time period which ranges anywhere between 5 to 10 years usually.

Let us take an example to understand how much you can get from Post Office RD:

Example

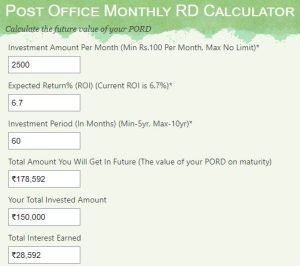

Srijan plans to invest Rs. 2500 per month in a recurring deposit scheme for 10 years at post office. The Post Office RD rate is 6.7% compounded quarterly (4times in a year).

The maturity value of the investment for Mr. Srijan using the moneycontain Post Office RD calculator is:

- Monthly investment amount: Rs. 2500

- Post Office Recurring Deposit Interest Rate: 6.7%

- RD Term: 5 years

- Total Investment: Rs. 1,50,000

- Total Interest Earned: Rs. 28,592

- Total Maturity Amount: Rs. 1,78,592

Post Office RD Calculator Formula:

The formula used to calculate returns from the post office RD account is as follows:

M =R[(1+i)n – 1]/1-(1+i)(-1/3)

where,

M = Total value of maturity

R = Amount of monthly deposits

n = Time period in years

i = interest rate offered

Let us understand this with an example. Suppose you want to deposit Rs 5,000 every month for 5 years in the post office RD that offers a 6.2% rate of interest. Here,

R = 5000

n = 5

i = 6.2

Putting these values in the formula we get:

M = 5000[(1+6.2)5 – 1]/1-(1+6.2)(-1/3)

M = Rs 3,52,462

Hence, you will get a maturity amount of Rs 3,52,462 on your total deposit of Rs 3,00,000, which means an interest of Rs 52,462.

How To Open Post Office RD Account?

You can visit yo your nearest post office in your area physically to open an account. However keep in mind to carry following documents to open it hassle free.

- Account opening form (filled and duly signed)

- Recent passport size photograph

- KYC Documents

- Individual & Company: PAN Card, Passport Copy, Aadhar Card, Voter’s ID, and Driving License

- HUFs: HUF declaration deed, bank statement of HUF, and self-attested PAN card

- Partnership Firms: Certificate of Incorporation, Partnership deed, and ID proofs of all authorized signatories.

Below is the eligibility criteria for opening post office RD accounts in India

- All Indian nationals over the age of 18 can open a Post Office Recurring Deposit account.

- Minors of age ten and above can open and operate the account jointly with a guardian.

- Parents or guardians can open this account on behalf of a minor child.

Note:- Any number of accounts can be opened

- Account can be opened by cash/cheque and in case of cheque the date of deposit shall be date of clearance of cheque.

- Minimum Amount for monthly deposit is Rs. 100 and above minimum in multiple of Rs. 10.

- Subsequent deposit shall be made up to 15th day of month, if account is opened up to 15th of a calendar month.

- Subsequent deposit shall be made up to last working day of month, if account is opened between 16th day and last working day of a calendar month.

Frequently Asked Question:

Is There any tax benefits of Post Office Recurring Deposits?

Investment in Post Office Recurring Deposit (PORD) qualifies for tax deduction up to INR 1,50,000 under Section 80C of the Income Tax Act. The interest income doesn’t attract any TDS.

However, income earned will be taxable in the hands of investors as per their respective income tax slabs.

Can I make advance deposits in my post office RD Account?

Yes, If an RD account is not discontinued can made advance deposit up to 5 years in an account. Rebate on advance deposit of at least 6 installments (inclusive of month of deposit), for Rs. 100 denomination rebate Rs. 10 for 6 month , Rs. 40 for 12 month. The advance deposit may be made at the time of opening of the account or any time thereafter.

Can I take loan on my post office RD Account?

Yes, After 12 installments deposited and account is continued for 1 year not discontinued depositor may avail loan facility up to 50% of the balance credit in the account. Loan can be repaid in one lump-sum or in equal monthly installments.

Interest on loan will be applicable as 2% + RD interest rate applicable to the RD account. Interest will be calculated from date of withdrawal to date of repayment. In case loan is not repaid till the maturity, loan plus interest will be deducted from the maturity value of the RD account.

Note:- Loan can be taken by submitting loan application form with passbook at concerned Post Office.

Can I close my post office RD Account before maturity?

Yes, PORD Account can be closed prematurely after 3 years from the date of account opening by submitting prescribed application form at concerned Post Office.

However, PO Savings Account interest rate will be applicable if the account is closed prematurely even one day before maturity. No premature closure of account shall be permissible until the period for which the advance deposits have been made.

Can I extend my Post Office RD even after 5 years?

Yes, account can be extended for further 5 years by giving application at concerned Post Office. Interest rate applicable during extension will be the interest rate at which account was originally opened.

Extended account can be closed any time during the period of extension. For completed years, RD interest rate will be applicable and for period less than a year, PO Savings Account interest rate will be applicable. RD account can be retained up to 5 years from the date of maturity without deposit also.

What happen If I default on my Post office monthly Rd?

If subsequent deposit is not made up to the prescribed day for a month, a default is charged for each defaulted month, default @ 1 rupee shall be charged for 100 rupee denomination account (proportionate amount for other denomination) shall be charged.

If in any RD account, there is monthly default, the depositor has to first pay the defaulted monthly deposit with default fee and then pay the current month deposit.

After 4 regular defaults, the account becomes discontinued and can be revived within two months from 4th default but if the account is not revived within this period, no further deposit can be made in such account and account became discontinued.

If there are not more than four defaults in monthly deposits, the account holder may, at his option, extend the maturity period of the account by as many months as the number of defaults and deposit the defaulted installments during the extended period.

Can I get a repayment on the death of account holder for PORD?

Yes, On the death of account holder nominee/claimant can submit claim at concerned Post Office to get the eligible balance of such RD account. After sanction of claim, Nominee/legal heirs can continue RD account till maturity by submitting application at the concerned Post Office.

Conclusion:

I hope you have tried calculating the returns by using the moneycontain Post Office RD calculator, doing a manual calculation takes much of time, therefore feel free to use the PORD calculator anytime you want.

Doing an investment with less risk may give less returns but what is most important is the peace of mind. That is why people usually makes investment in RD/FD rather than any other form of investments.

Checkout the impact of inflation on your returns as well as your life using moneycontain inflation rate calculator and calculate your future expenses easily.

You can also check Moneycontain Monthly SIP Calculator with inflation to know how much need to invest today to reach your future financial targets.

In case you are looking to buy a home than please check this ultimate guide on home loan and Moneycontain home Loan EMI calculator. It calculates your EMI’s as well as Interest amount and lot more.

If you want to explore the stock market and how does it work step by step than check moneycontain Free share market guide specially designed for beginners.

If, you have liked the content please do share it with your friends or on social media, as sharing do bring the good karma. If you have any questions or feedback you can leave them in comment box below.

Note: Please do not take this as any recommendation, to trade or invest. This is just for reference, to make you understand more about the usage of Post Office RD calculator and its importance, under no circumstances intended to be used or considered as financial or investment advice, a recommendation or an offer to sell, or a solicitation of any offer to buy any securities or other form of financial asset.

{kind=link}