What Is Post Office Monthly Income Scheme (POMIS) ?

Post Office Monthly Income Scheme POMIS is a government-promoted savings scheme offered by the Department of Post (DoP) or Indian Post.

Post office monthly income scheme popularly known as MIS (Monthly Income Scheme) offers individual common investors an opportunity to make a one time investment and get monthly fixed returns as an income.

POMIS is best suitable for those investors who are seeking fixed monthly income, as returns (%) in this scheme are fixed at least for a quarter and does not fluctuate much.

It is a government-promoted savings scheme offered by the Department of Post (DoP) or Indian Post, which makes it a 0% risk investment option.

The scheme’s interest rates are announced every quarter and is fixed and changed by the Central Government and Finance Ministry every quarter depending on the returns yielded by Government bonds of the same tenure. Moreover upon maturity of the scheme, you can choose to withdraw or reinvest the amount into the scheme.

Post office monthly income scheme provides guaranteed returns unlike market-linked instruments such as monthly SIP or LumpSum SIP where the returns are based on stock market behavior. It is one of the best monthly income plans for conservative low-risk investors.

POMIS gives investors monthly returns in the form of interest payments. GOI have kept the post office monthly income scheme interest rate at 7.6 % in current quarter starting from 01 July, 2025.

You can check the returns you can get on monthly basis as well as the total interest earned throughout tenure using moneycontain post office monthly income scheme calculator here.

Let us know in detail about the POMIS scheme, it’s features, comparison with other schemes, eligibility criteria, how to open an account and lot more step by step.

If you are looking for the best stockbroker I would recommend you to checkout this broker, or you can directly use the below link to open the account free of cost.

Post Office Monthly Income Scheme Details:

Few Point related to deposit in POMIS you should know :

- Account can be opened with minimum of Rs. 1000 and in multiple of Rs. 100.

- A maximum of Rs. 9 lakh can be deposited in a single account and 15 lakh in Joint account.

- In a joint account, all the joint holders shall have equal share in investment.

- Deposits/shares in all MIS accounts opened by an individual shall not exceed Rs. 9 lakh.

- Limit for account opened on behalf of a minor as guardian shall be separate.

- For calculation of share of an individual in joint account, each joint holder have equal share in each joint account.

The maximum limit of MIS in post office is Rs.9 lakhs in case of single account and Rs.15 lakhs in case of joint account (up to 3 joint holders) and for minor account (10 Years or Above) it is Rs.3 Lakhs from 01, April, 2023.

Type of Account | Maximum Limit |

Single Account | Rs. 9 Lakh |

Joint Account | Rs. 15 Lakh |

Minor Account | Rs. 3 Lakh |

Remember, there is no limit on the number of accounts held by individuals, there are limits on the maximum amount that can be cumulatively invested across all POMIS accounts.

The maturity period for POMIS is 5 Years (60 MONTHS) with 1 year of lock in period prior to that you cannot withdraw the amount deposited/invested.

- Account may be closed on expiry of 5 years from the date of opening by submitting prescribed application form with pass book at concerned Post Office.

- In case the account holder dies before the maturity, the account may be closed and amount will be refunded to nominee/legal heirs. Interest will be paid up to the preceding month, in which refund is made.

Post Office Monthly Income Scheme Interest Rates:

The Interest Rates on Post Office Monthly Income Scheme from 01 July, 2025 is 7.6% per annum payable monthly.

The Rate of interest(%) is fixed and changed by the Central Government and Finance Ministry every quarter depending on the returns yielded by Government bonds of the same tenure.

Below are the historical Post Office MIS Interest Rates*

Following Points to keep in mind while looking for interest rates in POMIS.

- Interest shall be payable on completion of a month from the date of opening and so on till maturity.

- If the interest payable every month is not claimed by the account holder such interest shall not earn any additional interest.

- In case any excess deposit made by the depositor, the excess deposit will be refunded back and only PO Savings Account interest will be applicable from the date of opening of account to the date of refund.

- Interest can be drawn through auto credit into savings account standing at same post office, or ECS. In case of MIS account at CBS Post offices, monthly interest can be credited into savings account standing at any CBS Post Offices.

- Interest is taxable in the hand of depositor

If you are looking for the best stockbroker I would recommend you to checkout this broker, or you can directly use the below link to open the account free of cost.

Post Office Monthly Incomes Scheme Benefits:

In my personal opinion POMIS plans are best way to get a fixed monthly income which can act as a steady flow of income for an individual. As the returns are guaranteed one can even reinvest the monthly income upon maturity.

Below are some of the major benefits to invest in an POMIS plan.

- Secured Returns – Post Office Monthly Income Schemes offer fixed interest income. As an investor one earns a fixed and safe flow of income every month. The current interest rate for year 2025 is 7.6% which is subject to change every quarter and ranges in between 6.6 to 7.6%* usually.

- Reinvestment Option – MIS scheme of post office allows you to reinvest the monthly income which you get in form of interest even after maturity. Upon maturity, you may also choose to reinvest the corpus in the same scheme for another five years to get major benefits.

- Nomination Facility – Nominee facility is available with POMIS plan and can be updated later after opening an account by a beneficiary (i.e. a family member), however one can only claim the benefits after the demise of the account holder.

- Easy Transfer Facility – POMIS accounts can be freely transferred from one Post Office to another.

- For Minors – Even a minor aged 10 years or above can avail the Post Office Monthly Income Scheme Account. On turning 18 years, he or she will be asked to convert his/her minor account to an adult account.

- Quick Withdrawal – The Post office credits proceeds directly to the investor’s post office savings account on a monthly basis by ECS/CBS.

- Interest After Maturity – Post Office Monthly Income Scheme accounts can continue to earn interest for up to 2 years after account maturity if proceeds/investments are not withdrawn by the investor. The applicable rate will be the same as that of a standard Post Office savings account

POMIS Disadvantage:

- Bonus – No bonus available on accounts opened on or after 1st December 2011 for Post Office Monthly Income Scheme. Accounts opened earlier were eligible for a 5% bonus on deposit amount.

- Taxability – MIS plan doesn’t come under the Section 80C of the Income Tax and it is subject to taxation.

- TDS – TDS (Tax Deducted at Source) is not applicable

How To Open Post Office Monthly Incomes Scheme Account ?

To open a POMIS account you first need to visit the nearest post office in your area as it can only be through post office.

You must have a Post Office savings account in order to apply for MIS scheme, incase you do not have one, open the savings account at post office first and than you need to fill in another form to open a MIS.

Below is Step by Step processes for opening a POMIS account

- You can get an application form from your Post Office or Click here to download POMIS Account application form

- Fill and submit the form along with the copies of all the required documents at the post office.

- Note: You must carry the original documents for verification

- Mention the Name, DOB and Mobile no. of the nominees (if any) However, the nominee details can be added at a later point as well. Additionally, one needs to get signatures of a witness or a nominee(s) on the form.

- All the documents should be self-attested

- Deposit the cash or cheque with minimum of Rs. 1000 and in multiple of Rs. 100. If the cheque is a post-dated cheque, then the date of the account opening would be the date mentioned on the cheque.

Note: The interest disbursement on the investment amount is one month from the account opening date.

Which Documents Needed To Open POMIS Account?

Following are the documents that one requires to open a POMIS account:

- Two Passport size photographs

- Address Proof

- Identify Proof (Aadhar Card, Voter ID, Pan Card, Ration Card, Driving License or Passport, etc.) Make sure you keep the original copies of the proofs as they are necessary for verification.

Can I Close My POMIS Account Early ?

Premature withdrawal /closure of POMIS account before maturity period (5 years) is allowed subject to following terms and conditions:

- In case of premature withdrawal between 1 to 3 years of account opening, a 2% discount on deposit is applicable

- In case of premature withdrawal between 3 to 5 years of account opening, 1% discount on deposit is applicable

- No deposit shall be withdrawn before the expiry of 1 year from the date of deposit.

- If account is closed after 1 year and before 3 year from the date of account opening, a deduction equal to 2% from the principal will be deducted and remaining amount will be paid.

- If account closed after 3 year and before 5 year from the date of account opening, a deduction equal to 1% from the principal will be deducted and remaining amount will be paid.

- Account can be prematurely closed by submitting prescribed application form with pass book at concerned Post Office.

If you are looking for the best stockbroker I would recommend you to checkout this broker, or you can directly use the below link to open the account free of cost.

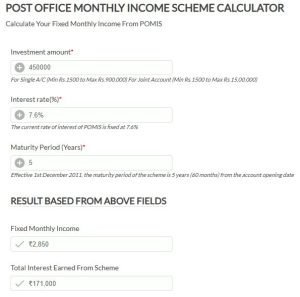

How Much Can I Get Monthly Investing In POMIS Account ?

If you wish to invest let say Rs.4,50,000 assuming the average rate of interest for the entire tenure of 5 years is 7.6%, you can get a fixed monthly income of Rs.2,850 and the total interest earned from the scheme will be Rs.1,71,000.

Check out the below image from moneycontain post office monthly income scheme calculator:

Using the Moneycontain Post Office Monthly Income Scheme calculator, you can quickly and easily calculate the Monthly Interest. The post office monthly income scheme MIS interest rate calculator need the user to input the following details:

Investment Amount: It is the total corpus amount invested in the Post Office Monthly Income Scheme.

Interest Rate: The rate of interest at the time of opening the account.

Maturity Period: It is the duration of the investment which is currently 5 years.

If you’re looking for a modern, feature-rich, and trader-friendly platform, Dhan is easily one of the best choices available today. From zero account opening charges to advanced tools like native TradingView, options strategy builder, and free API access, Dhan is clearly built with the modern Indian trader in mind.

Whether you’re an intraday trader, an options strategist, or a long-term investor, Dhan offers the perfect blend of speed, simplicity, and smart technology — without burning a hole in your pocket.

Why wait? Open your Dhan account now and take control of your trading journey with confidence.

👉 Click here to get started with Dhan

Open a Free Dhan Trading & Demat Account

Dhan offers cutting-edge tools for fast, powerful, and informed trading:

- ✅ Zero brokerage on delivery trades

- ✅ Auto-detection of candlestick patterns on charts

- ✅ Advanced Option Chain with Greeks, Max Pain, PCR & more

- ✅ Pre-built & custom Option Strategy Builder (Free)

- ✅ 20 Depth Market Data and Flash Trade execution

- ✅ Margin Trading Facility (MTF) with 4X leverage (75%)

- ✅ 3 Platforms: Mobile App, Web App & Dedicated Options App

- ✅ ScanX Screener: stock insights, trends & news

- ✅ Advanced orders: Trailing SL, Iceberg, Forever Orders

- ✅ Instantly pledge 1,500+ stocks for options margin

- ✅ Trade commodities: Gold, Silver, Crude, Natural Gas

- ✅ Fundamental + Technical analysis across all platforms

No paperwork. Zero account opening charges. Setup in minutes.

Can I withdraw money from POMIS account after the tenure?

Money can be drawn through auto credit into savings account standing at same post office you have account, or through ECS ((Electronic Clearing System)).

In case of MIS account at CBS Post offices, monthly interest can be credited into savings account standing at any CBS Post Offices.

Can I transfer my POMIS account?

To transfer POMIS account you need to visit your post office and make a request informing about the post office where you need to transfer the account. Your account can be transferred from one post office to another for absolutely free.

For POMIS account transfer, you need to have the transfer application form. The transfer form name is Form SB 10(b) and it is available at any post office. You can also download this form online.

You need to fill the form with basic details like POMIS account number, branch, bank details like bank account number, ifsc code, etc., and signatures of all the account holders.

Then the passbook and the form have to be submitted. The Postal Assistant (PA) in the existing branch will give an acknowledgment slip and forward it to the post office in the new location where the investor wants to transfer the account.

The same slip should be presented to the PA of the branch where the account has to be transferred. Then the investor will get the new passbook with the old balance.

What happens If I do not withdraw the funds from POMIS even after 5 years?

After the maturity of 5 years, if you do not withdraw the amount, then he will continue to earn a simple interest for up to 2 years (as per the post office savings account interest rate).

Account may be closed on expiry of 5 years from the date of opening by submitting prescribed application form with pass book at concerned Post Office.

Is there any TDS Applicable For POMIS Account?

There is no TDS (Tax Deduction at Source) for interest one earns in POMIS, However, the interests earned are taxable.

Does POMIS offer any tax rebate?

No, unfortunately POMIS does not offer any tax benefits under Section 80C of the Income Tax Act, 1961.

If you are looking for the best stockbroker I would recommend you to checkout this broker, or you can directly use the below link to open the account free of cost.

Is Nominee Facility Available In POMIS Account ?

Yes, the post office MIS allows you to have a nominee against the account. In case the account holder dies before the maturity, the account may be closed and amount will be refunded to nominee/legal heirs.

Interest will be paid up to the preceding month, in which refund is made.

POMIS Comparison With Other Schemes:

There are varieties of schemes available in market, choose the right one which suits your need. Below image tells you comparison between different saving schemes such as POMIS vs Bank FD vs NSC

Likewise, if we compare post office monthly income scheme with private investments funds such as mutual fund schemes or Insurance Schemes, we may expect better returns (subject to market) moreover the investment amount in such scheme is not limited as in case of post office MIS.

Other Than MIS there are other types of accounts one can open with the post office or India Post:

- Post Office Savings Account

- Senior Citizens Savings Scheme

- Public Provident Fund Account

- Sukanya Samriddhi Yojana

- 5-Year Post Office Recurring Deposit Account

- Post Office Time Deposit Account

- National Savings Certificate

The rate of interest varies across types of scheme, having said that every scheme does have guaranteed returns which is great. They do have different maturity and lock in period as well ranging from 5 to 18 years.

However, the taxation for each of these investment plans is also different. Below image represent some of the schemes with interest and TDS.

If you are looking for the best stockbroker I would recommend you to checkout this broker, or you can directly use the below link to open the account free of cost.

Conclusion:

If you are someone who is looking for a fixed monthly income without worrying about the ups and down of stock market related schemes, than Monthly Income Scheme in Post Office is the best choice.

It’s backed by government and have assured returns which makes it even more secure.

If, you have liked the content please do share it with your friends or on social media, as sharing do bring the good karma. If you have any questions or feedback you can leave them in comment box below.

National Pension Scheme (NPS) – Details, Benefits, Returns, Interest, Features

National Savings Certificate – NSC Interest Rates, Features, Returns, Scheme Details

Want to know how much you need to save and invest every month for your retirement goal then do check moneycontain retirement calculator with inflation here.

If you’re looking for a modern, feature-rich, and trader-friendly platform, Dhan is easily one of the best choices available today. From zero account opening charges to advanced tools like native TradingView, options strategy builder, and free API access, Dhan is clearly built with the modern Indian trader in mind.

Whether you’re an intraday trader, an options strategist, or a long-term investor, Dhan offers the perfect blend of speed, simplicity, and smart technology — without burning a hole in your pocket.

Why wait? Open your Dhan account now and take control of your trading journey with confidence.

👉 Click here to get started with Dhan

Open a Free Dhan Trading & Demat Account

Dhan offers cutting-edge tools for fast, powerful, and informed trading:

- ✅ Zero brokerage on delivery trades

- ✅ Auto-detection of candlestick patterns on charts

- ✅ Advanced Option Chain with Greeks, Max Pain, PCR & more

- ✅ Pre-built & custom Option Strategy Builder (Free)

- ✅ 20 Depth Market Data and Flash Trade execution

- ✅ Margin Trading Facility (MTF) with 4X leverage (75%)

- ✅ 3 Platforms: Mobile App, Web App & Dedicated Options App

- ✅ ScanX Screener: stock insights, trends & news

- ✅ Advanced orders: Trailing SL, Iceberg, Forever Orders

- ✅ Instantly pledge 1,500+ stocks for options margin

- ✅ Trade commodities: Gold, Silver, Crude, Natural Gas

- ✅ Fundamental + Technical analysis across all platforms

No paperwork. Zero account opening charges. Setup in minutes.

You can also check my reviews on best brokers in India

Incase you are looking for any Home loan or want to calculate the monthly EMI, than do check moneycontain free home loan EMI calculator.

Note: Please do not take this as any recommendation, to trade or invest. This is just for reference, to make you understand more about post office monthly income scheme and its importance, under no circumstances intended to be used or considered as financial or investment advice, a recommendation or an offer to sell, or a solicitation of any offer to buy any securities or other form of financial asset.

Please do your own research and make investment. Moneycontain will not be responsible for any of your losses at all. The point made is for educational purpose only. All investments are subject to risks, which should be considered prior to making any investments.

{kind=link}