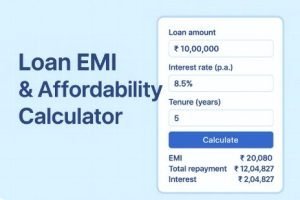

Are you planning for your dream vacation, home renovation, wedding, or want to pay your children school/college fees, personal loan EMI calculator can be a useful tool to find out the exact monthly EMI installments you may need to pay to your lender.

Moneycontain Personal loan EMI calculator will help you to find out exact monthly EMI installments, total interest that you need to pay on the principal or loaned amount as well as the total amount payable at the end of the loan tenure.

Just enter the personal loan amount, interest rate% charged on loan by your lender ( Bank, NBFC etc.) and tenure in months in below personal loan calculator, get all the information required within seconds.

What Is Personal Loan?

Personal loan is a kind of unsecured loan which does not require any security or collateral such as gold, property, shares or any other asset. In other words you do not have to provide any security or collateral to get a personal loan.

This is also the reason why personal loans carry a relatively higher rate of interest in comparison to secured loans, where there is some form of security or collateral submitted by the borrower.

A personal loan is useful for any emergency work you want to do, which means you can use that money in any work you have, such as for bill payments of hospitals, wedding expenditure, home renovation, paying for your children fees, etc. the lender does not ask about the work that is why it is called personal loan.

Getting a personal loan is easier if you someone who is currently working in any private MNC or any other government job.

A personal loan approval is depended on your monthly salary, how long you have been working ,your company reputation, whether you already have ongoing EMI’s to pay, as well as your credit score.

This does not means a self-employed person can’t get the personal loan, a self-employed applicants with a stable source of income can also avail personal loans from banks, NBFCs and other lenders at lower interest rates from market.

Important Terms Related To Personal Loan:

- Loan – A certain amount that is borrowed, and is expected to be paid back with interest.

- Principal – The total money owed or the total remaining balance of your loan.

- Interest – Interest is the cost of borrowing money for your loan from lenders.

- Loan Term/Tenure – The total amount of time it will take to pay off a loan as agreed upon with the lender.

- EMI – It is the total amount payable every month until the loan has been fully repaid.

Different Type Of Personal Loan Interest Rates?

Interest is the cost of borrowing money for your personal loan from lenders.

Applicants for personal loans have to pay back at Adjustable also known as floating or fixed interest rates and other payment terms set by the bank or non-banking financial company. The interest rates policies are set and governed by RBI.

1.Fixed Interest Rates: As the name suggests, in fixed interest rate the rate of interest remains same throughout the loan tenure. Hence, monthly EMI amount also remain fixed throughout the loan repayment period.

2.Adjustable/Floating Interest Rates: This type of interest rates are usually depends on either the internal benchmark set by the lender or it may also depends on ongoing market conditions.

Therefore, floating interest rate is likely to change systematically which may cause increase/decrease in loan tenure or monthly EMI payouts depending on the movement of the interest rate up and low.

Usually, banks and NBFC’s charges fixed interest rate for personal loans.

Lower the interest rates for your personal loan, lower will be the total amount you pay.

For example: suppose you bought a personal loan of ₹2,00,000 At, Interest rate of 12 % with tenure (in years) 3 than your EMI for every month with Principal & Interest is ₹6,642

The formula use to calculate EMI is:

The formula –

EMI = [P x R x (1+R) ^N]/ [(1+R) ^ (N-1)]

EMI |

Equated Monthly Payment |

P |

Principal amount |

R |

Rate of interest |

N |

Tenure |

EMI stands for equated monthly instalment. It is the total amount payable every month until the loan has been fully repaid. EMI consists of a principal amount and interest on the loan.

The principal amount is the original loan amount given to you by the bank, on which the interest will be calculated.

How is principal and interest split in EMI?

Personal loan, EMI comprises two components, such as principal and interest rates. The interest component is higher in the initial years and reduces over the years.

When you pay an EMI, all the interest is first paid, and the remaining amount is considered as principal. Every month the interest is calculated on outstanding amount.

Suppose you have taken Rs. 1 Lakh loan for 12 months at 12% rate. The EMI for the loan will be Rs. 8,885.

Interest component in 1st EMI = (12/12*100)*1,00,000 = Rs. 1000

Principal component in 1st EMI = 8,885 – 1,000 = 7,885

In next EMI, the interest amount will be calculated on an outstanding principal of 1,00,000 – 7,885 = Rs. Rs. 92,115. By the end of the tenure, the interest component will come down to zero and the amount you pay as EMI is the remaining principal. This is how interest and principal split in EMI.

What Is Personal Loan EMI Calculator Formula?

It becomes difficult to calculate your loan EMIs manually as the process is time taking and difficult.

If you want to calculate your EMI you only need to enter your loan amount, interest rate to be charged and tenure of loan. The formula used by personal loan calculator is:

P*r* (1+r)^n/([(1+r)^n]-1)

In above formula, P is the loan amount that you want to borrow

R is the rate of interest per month

N is the tenure of loan repayment in months

When you use the above formula, you will get the same result that you will get in the Personal loan emi calculator. It is advised to use personal loan emi calculator as it is very easy and time saving process and helps you in calculating your EMI in seconds.

Use moneycontain personal loan calculator to get the complete schedule of your EMIs along with principal and interest component in it.

How to calculate personal loan EMI in Excel?

If you know little MS-Excel you can calculate personal loan EMI by following formula:

PMT (rate, nper, pv)

Where,

rate = Personal loan interest rate (in percentage)

nper = Loan tenure in months i.e. number of EMIs payable

pv = Loan principal (present value)

How Accurate Is Moneycontain Personal Loan EMI Calculator?

Moneycontain personal loan emi calculator is as accurate as any other prominent banking website such as Kotak Mahindra bank, below is the snapshot I have taken from their website and with similar values I have entered that in moneycontain personal loan emi calculator, you can check the results for both:

What Is Personal Loan Eligibility Criteria?

As mentioned above there are many factors which effects the approval for the personal loan and its individual specific, having said that below are some of the points that affects the most:

Age: A younger individual has a higher chance of getting a higher loan amount approved as compare to an older individual, as a younger person will have more years ahead and with time his chances of earning may increase.

Income: Your income is also an important factor in your personal loan eligibility. Higher your income, more will be your scope of borrowing. Minimum Net monthly salary of Rs. 20,000/- is required.

Salaried/Self-employed: Your occupation also have a role to play in how much and how soon will you get approved, employees of either MNCs, Public and Private limited companies with a minimum age of 21 years and maximum age of 58 years are eligible for a personal loan.

Whereas for self-employed they have to show their regular stream of income and its sources like business or any other.

Income stability: An individual with a steady and stable income (government) is more likely to get a loan than one with an irregular income (private).

Expenses: Your monthly expenses will also be an factor for you to decide how much loan you can afford. So try to keep it low.

Existing EMIs: If there is already an existing loan, than you have to be balance and get rid of that as soon as possible, however if you have paid it without any default this shows the credibility to the lender.

Credit score: A higher credit rating makes the loan approval process faster and easier and vice versa.

Rejected loan applications: If you have had prior loan applications on which you have defaulted, it will negatively impact your credit score, thus reduces the chances of fresh new loan.

How To Reduce Personal Loan EMI Amount?

If you want to reduce your overall EMI you need to keep following things in mind:

- Loan principal – As a rule of thumb, the higher the amount borrowed as a personal loan, the higher will be your EMI as long as the tenure and interest rate remains constant.

- Interest rate – The higher the interest rate, the higher will be your individuals EMI pay out as well as the total interest payable on your personal loan.

- Tenure – When a longer tenure is opted for, individual EMI payments will decrease as compared to a shorter tenure for the same loan. But a longer tenure also results in higher total interest payable over the loan tenure.

How Personal Loan Prepayment Works?

There are two ways a loan prepayment works:

Full Prepayment:

As discussed above, EMI comprises two components, such as principal and interest rates. The interest component is higher in the initial years and reduces over the years, so if the prepayment in full can be done somewhat early into the tenure of the loan, a customer may save a lot on the interest.

A personal loan or for that matter any other type of loan, usually has a lock in of about one year after which the entire outstanding amount can be prepaid.

For example, if the personal loan is for Rs. 1 lakh at an interest rate of 15% and for a term of 2 years, the monthly EMI comes to Rs. 4,848.

At the end of the first year the customer would have paid Rs. 46,272 towards premium and Rs. 11,904 as interest. If the customer decided to prepay the full amount now, he would stand to pay Rs.4,464 less in the form of interest.

Now, suppose the tenure is much longer let say instead of two year if it was 4 or 5 years for the same amount and rate of interest, the earlier you would have made the full prepayment the more you would have saved the interest.

However, there are often prepayment penalties of about 3 to 4% on outstanding principal amount, linked with paying off personal loans ahead of time, it is generally cheaper and better to prepay your loan as compared to continuing to the longer tenure.

As in case of above example 3% of Rs.53,720 is about Rs. 1,611 even if you deduct that from interest amount you would still have saved around Rs.2852.

Prepayment of an ongoing personal loan may not have an immediate effect on your credit rating, however in the long term a full prepayment strengthen up your credit rating for sure.

Part Prepayment:

Part payment of a personal loan helps in reducing the burden of EMI as well as lowering down the interest charges on the principal amount. So, when you have a lump sum amount in between the loan tenure it is a food option to pay-off some part even if it is not equivalent to the entire principal outstanding loan amount.

However, it is important to keep in mind that only when you make a significant amount of lumpsum money as part payment, you EMI and interest will lower down.

Part pre payment of a loan has no effect on your credit rating, still it reduces your total loan burden, which in turn should help you to pay off the loan completely in the given tenure. Moreover it mark’s yourself as a better borrower than other others.

Which Bank/NBFC Charges Lowest Personal Loan Interest Rates in India:

Check out the list of lowest personal loan interest rates offered by major banks and Non-Banking Financial Companies (NBFCs) in India below:

FAQ on Personal Loan:

What is the personal loan eligibility for salaried employees?

Loan eligibility for salaried employees depends on various factors such as:

What is the minimum and maximum age to get a personal loan?

The minimum age limit to apply for a loan should be 21 years. Maximum age can go up to 60 years (salaried employees) and 65 years (self employed professionals) at the time of loan maturity. However, age varies from bank to bank.

Can I get a Personal loan of 1 lakh?

Of Course you can, if you are salaried person have minimum Rs.20,000 and working experience of at least a year, whereas if you are self-employed you need to show the source of income to get the loan credited.

How does my income affect my loan eligibility?

Your monthly income to get a personal loan should be at least ₹ 2o,000. Having said that, some banks give loans to individuals with salary more than ₹ 25,000, some allow about Rs.18,000 as minimum benchmark.

There is something called as ratio of your fixed obligations to your monthly income. These fixed obligation can be a rented house, your other expenses, your marital status, any other EMI etc.

Suppose, your income is ₹ 30,000, the bank calculates your eligibility such that fixed obligations do not exceed 60% of your income. Which simply means all your expenses should come under 60% of your expenses.

In other words higher the income, and lower expenses the better are the chances to get high loan amount.

Does my company name affect my eligibility for a personal loan?

Yes, company profile/name/brand whatever you call it, affects your loan eligibility. Good company such as MNC’s or a government or semi-government profile and high salary increase your eligibility to get a personal loan at a low rate of interest.

Do my existing loan affect my personal loan eligibility?

If you are already paying an EMI for any existing loan then your eligibility for the new loan applied will be comparatively low, but it also depends on your salary and expenses.

How to improve my eligibility for personal loan?

You can improve your eligibility for a personal loan by doing the following things:

Can I change my personal loan EMI date? Are there any charges applicable?

Yes, it is possible to change the Installment date. The dates are available between 2nd and 10th of every month. Changing of EMI date will attract rescheduling charges and PDC Swap charges* per instance plus applicable GST.

How long does bank take to approve a personal loan?

Once you submit your application form and the required documents as per Bank’s criteria, you can expect our approval and disbursal of your personal loan within 10 working days provided everything is in order.

How much personal loan can I get?

Banks ask for a minimum income of ₹ 20 to 25,000 for a personal loan. However, some banks give loans for a salary less than ₹ 20,000. Your loan eligibility is calculated based on the ratio of your fixed obligations to your monthly income also known FOIR.

If your income is less than 30,000, then the maximum obligations cannot exceed 50% of your monthly income. However, for a higher income, the obligations to income ratio can go up to 65%. If you have a higher income, then there are better chances to get a higher loan amount.

How much credit score required to get a personal loan?

This depends from bank to bank however, Make sure to keep your credit score above 700, as most of the borrowers accepts the application at this score.

What are the documents required for a personal loan?

The following documents are required for applying for a personal loan:

- Application Form

- 2-4 Photograph

- Identity Proof

- Residence Proof

- Age Proof

- Signature Proof

- Ownership Proof

- Income Details

- Bank Account Statements

How much loan can I get if my salary is 20,000?

The personal loan amount depends on fixed obligation to income ratio FOIR and multiplier. The lower of these two factors are contemplate as the eligible loan amount.

Let us suppose the bank gives a loan at a FOIR of 50%, and the maximum multiplier is 20, and you do not have any ongoing EMI.

The maximum amount you can pay as EMI for personal loan is ₹ 20,000*50% = ₹ 10,000. If you take a personal loan for a maximum of 5 years, then your loan amount will be ₹ 10,000*12*5 = ₹ 600,000.

However, the multiplier is 20, then the loan amount will be ₹ 20,000*20 = 4,00,000. Therefore, the amount you will get on ₹ 20,000 salary is ₹ 4,00,000.

Apart from income, eligibility depends on various other factors so do not take it as a thumb rule.

How are loan prepayment penalties calculated?

Loan prepayment penalties are charged at 3-4% on the remaining outstanding amount, so suppose if the remaining principal amount on your loan is Rs.100,000 than it will be 3k to 4k.

Is it better to reduce EMI or tenure?

It is always advisable to reduce the tenure not the EMI, the earlier you pay-off your debt or loan the better it is, as you will be saving a lot of interest charged in total to your loan amount.

Can I pay more than my EMI in personal loan?

Yes, you can pay more than the EMI, which is known as part prepayment, this also helps in overall tenure reduction which helps in saving interest.

Can we pay prepayment in personal loan?

Yes, you can make a prepayment in personal loan, but most of the banks will only allow it either 6 months or 1 year completion not before that.

Can EMI be reduced?

Yes EMI, can be reduced but it is not advisable as the lower EMI will make the longer tenure of the loan which make the more interest .

Conclusion:

I hope personal loan EMI calculator with other important information would have helped you and saved your time.

If you ask me personally, I would advise anyone, any-day not to go for any loan until it is very critical for you.

Instead, save money or invest in other financial assets (like gold, fixed deposits, SIP, mutual funds, stocks indexes as long as you can.

Buy anything when you have that amount in your hand instead of taking any loan.

Having said that there is no guarantee as such, I just wanted to present you the another point of view, its your hard earned money, so do proper research before taking any decision.

In case you want to know how much you need to save every month to reach your financial goals check out Moneycontain Monthly SIP Calculator with inflation here.

Do you know the concept of present value of your future money, if not then you should.

Just like 100 rupees in your pocket today will not have value of 100 rupees after 5 years, similarly 100 rupees you receive in future, invested today won’t have the same value. ?Confused??

Check moneycontain present value calculator and ultimate guide on NPV here.

If you have to analyze, what would be the value of money that you have today sometime in the future, then you need to move the ‘money today’ through the future i.e. future value of that money.

This is a much read from my end to better understand the flow of money.

If you are looking for making an FD fixed deposit than do check best banks in India with Highest FD returns and calculate the value of your FD Moneycontain free FD calculator with inflation.

Checkout the impact of inflation on your returns as well as your life using moneycontain inflation rate calculator and calculate your future expenses easily.

Incase you are looking for any Home loan or want to calculate the monthly EMI, than do check moneycontain free home loan EMI calculator.

If, you have liked the content please do share it with your friends or on social media, as sharing do bring the good karma. If you have any questions or feedback you can leave them in comment box below.

{kind=link}