Moneycontain NPS Calculator is useful for not only knowing the total corpus or pension wealth created but it is also helpful in knowing how much pension per month you will get from NPS. National Pension Scheme in short known as NPS is a low cost, tax-efficient, flexible and compact retirement savings account.

Under the NPS, the individual contributes to his retirement account and also his employer can also co-contribute for the social security and welfare of the individual.

This means you as an individual investor one can opt for NPS as well as your employer incase you work somewhere can also make the contribution from your behalf.

Online NPS calculator is a great tool which comes handy when you want to check how much you can expect at the retirement i.e. 60 years of age, NPS Calculator gives you an estimate of total pension corpus you will have at the end of the tenure, it shows how much you can get per month in form of pension amount, as well as it tells you how much you can withdraw from NPS Account as a lumpsum amount at the maturity.

To use below NPS Calculator you need to enter following details:

- Your current age, This should be 18 or above and 59 or below

- Your monthly contribution towards NPS (It can be as low as Rs.1000 per year)

- The expected rate of return (%) from NPS (10 to 15% p.a. is average return historically), also keep in mind that return under NPS is market driven. Hence, there is no guaranteed/defined amount of return.

- You will also need to enter the Percentage of Annuity you need to purchase, This should be 40% or above, this is the percentage of amount i.e. pension fund that you would like to reinvest to buy an annuity or maturity. In simple words annuity means the amount the subscriber of NPS scheme will receive per month after retirement from the ASP (Annuity Service Provider).

- Keep in mind that the percentage of accumulated funds reinvested to purchase annuity cannot be less than 40%. However incase of premature exit of scheme i.e. before 60 years of age, the minimum percentage of fund to be reinvested to purchase annuity should be 80% or above.

- At last you need to enter the expected rate of annuity, i.e. the amount of annuity you want to get from your pension every month. This should be in range of 4 to 10 %.

The NPS Calculator will show you the result based on enter field, You will be able to find following answer:

- How many years of contribution you have made to NPS?

- How much total corpus as an pension created from NPS?

- Your total invested amount in NPS

- The total interest you have earned under the National Pension Scheme

- How much amount have been reinvested as an annuity?

- The total Lumpsum amount you have withdraw after the completion of the scheme i.e. 60 years of age.

- How much pension per month you will get from NPS?

So, go ahead and try using the below moneycontain free NPS calculator and checkout how much you ca expect per month as a pension.

How many years will I get a pension in the NPS after the age of 60?

You may be thinking alright I find the amount I may get every month as a pension, but for how long. To answer this first you my need to understand different annuity options available under different ASP (Annuity service providers), this simply means while taking the annuity at the time of exit from NPS you will be provided different choices.

The different type of Annuity options in NPS:

- Annuity/ pension payable for life at a uniform rate.

- Annuity payable for 5, 10, 15 or 20 years certain and thereafter as long as the annuitant is alive.

- Annuity for life with return of purchase price on death of the annuitant.

- Annuity payable for life increasing at a simple rate of 3% p.a.

- Annuity for life with a provision of 50% of the annuity payable to spouse during his/her lifetime on death of the annuitant.

- Annuity for life with a provision of 100% of the annuity payable to spouse during his/her lifetime on death of the annuitant.

- Annuity for life with a provision of 100% of the annuity payable to spouse during his/ her life time on death of annuitant. The purchase price will be returned on the death of last survivor.

Subscriber can opt for any of the above annuity variant at the time of exit.

Now, that you have calculated the returns using NPS Calculator from National Pension Scheme and also know for how long the pension will be given to you, it is time to know in detail about the NPS.

We will go step by step to know everything related to the NPS, having said that you can use above table of contents to checkout topics which interests you more.

What Is NPS (National Pension Scheme)?

National Pension System (NPS) is a pension cum investment scheme launched by Government of India (GOI) to provide old age security to Citizens of India. It brings an attractive long term saving avenue to effectively plan your retirement through safe and regulated market-based return.

The Scheme is regulated by Pension Fund Regulatory and Development Authority (PFRDA). National Pension System Trust (NPST) established by PFRDA is the registered owner of all assets under NPS.

Under NPS, individual savings are pooled in to a pension fund which are invested by PFRDA regulated professional fund managers as per the approved investment guidelines in to the diversified portfolios comprising of Government Bonds, Bills, Corporate Debentures and Shares.

These contributions would grow and accumulate over the years, depending on the returns earned on the investment made.

At the time of normal exit from NPS, the subscribers may use the accumulated pension wealth under the scheme to purchase a life annuity from a PFRDA empaneled Life Insurance Company apart from withdrawing a part of the accumulated pension wealth as lump-sum, if they choose so.

How NPS works?

Upon successful enrolment of an NPS account, a Permanent Retirement Account Number (PRAN) is allotted to the subscriber under NPS.

Once the PRAN is generated, an email alert as well as a SMS alert is sent to the registered email ID and mobile number of the subscriber by NSDL-CRA (Central Record Keeping Agency).

Subscriber contributes periodically and regularly towards NPS during the working life to create the corpus for retirement.

On retirement or exit from the scheme, the Corpus is made available to the Subscriber with the mandate that some portion of the Corpus must be invested in to Annuity to provide a monthly pension post retirement or exit from the scheme.

What is Annuity in NPS?

In the context of NPS, Annuity refers to the monthly sum received by the Subscriber from the Annuity Service Provider (ASP). A percentage of the pension wealth as decided by the Subscribers (minimum 40% & 80% in case of Superannuation & Pre-mature Exit respectively) is utilized for purchase of Annuity from the empanelled Annuity Service Providers.

Who are the Annuity Service Providers under NPS and their names?

Indian Life Insurance companies who are licensed by Insurance Regulatory and Development Authority (IRDA) are empanelled by PFRDA to act as Annuity Service Providers to provide annuity services to the subscribers of NPS.

Currently, the following are the ASPs are empanelled by PFRDA and the empanelment process is an ongoing process and the list of ASPs may increase in future.

1. Life Insurance Corporation of India

2. SBI Life Insurance Co. Ltd.

3. ICICI Prudential Life Insurance Co. Ltd.

4. Star Union Dai-ichi Life Insurance Co. Ltd.

5. HDFC Standard Life Insurance Co. Ltd

Who all Can Invest in NPS?

Basically anyone whether Indian resident or NRI in age group of 18-60 years can invest through NPS. Having said that one also need to know NPS can be broadly classified into two categories and it is further customised for different sectors as mentioned below:

- Government Sector:

- Central Government:

The Central Government had introduced the National Pension System (NPS) with effect from January 1, 2004 (except for armed forces). All the employees of Central Autonomous Bodies who have joined on or after the above mentioned date are also mandatorily covered under Government sector of NPS. Central Government/CABs employee contributes towards pension from monthly salary along with matching contribution from the employer. - State Government:

Subsequent to Central Government, various State Governments adopted this architecture and implemented NPS with effect from different dates. A State Autonomous Body (SAB) can also adopt NPS if the concerned State Government/UT have adopted the NPS architecture and initiated implementation of the same. State Government/SABs employees also contribute towards pension from monthly salary along with matching contribution from the employer.

- Central Government:

- Private Sector (Non-Government Sector):

- Corporates:

NPS Corporate Sector Model is the customized version of NPS to suit various organizations and their employees to adopt NPS as an organized entity within purview of their employer-employee relationship. - All Citizens of India:

Any individual not being covered by any of the above sectors has been allowed to join NPS architecture under the All Citizens of India sector from May 01, 2009.

- Corporates:

Who are Eligible For NPS?

Under All Citizen Model

A citizen of India, whether resident or non-resident, subject to the following conditions:

Applicant should be between 18 – 60 years of age as on the date of submission of his/her application to the POP Points of Presence/ POP-SP Points of Presence service provider.

Can an NRI Open NPS?

Yes, an NRI can open an NPS account. Contributions made by NRI are subject to regulatory requirements as prescribed by RBI and FEMA from time to time. However, OCI (Overseas Citizens of India) and PIO (Person of Indian Origin) card holders and HUFs are not eligible for opening of NPS account.

Can I open multiple NPS accounts?

No, opening multiple NPS accounts for an individual is not allowed under NPS. However an Individual can have one account in NPS and another account in Atal Pension Yojna.

What are Benefits of NPS?

- Flexible- NPS offers a range of investment options and choice of Pension Funds (PFs) for planning the growth of the investments in a reasonable manner and monitor the growth of the pension corpus. Subscribers can switch over from one investment option to another or from one fund manager to another.

- Simple – Opening an account with NPS provides a Permanent Retirement Account Number (PRAN), which is a unique number and it remains with the subscriber throughout his lifetime. The scheme is structured into two tiers:

- Tier-I account: This is the non-withdrawable permanent retirement account into which the regular contributions made by the subscriber are credited and invested as per the portfolio/fund manager chosen of the subscriber.

- Tier-II account: This is a voluntary withdrawable account which is allowed only when there is an active Tier I account in the name of the subscriber. The withdrawals are permitted from this account as per the needs of the subscriber as and when required.

- Portable- NPS provides seamless portability across jobs and across locations. It would provide hassle-free arrangement for the individual subscribers while he/she shifts to the new job/location, without leaving behind the corpus build, as happens in many pension schemes in India.

- Well Regulated- NPS is regulated by PFRDA, with transparent investment norms, regular monitoring and performance review of fund managers by NPS Trust. The account maintenance costs under NPS are the lowest as compared to similar pension products across the globe. While saving for a long-term goal such as retirement, the cost matters a lot as the charges can shave off a significant amount from the corpus over 35-40 years of investment period.

- Dual benefit of Low Cost and Power of compounding: Till the retirement, pension wealth accumulation grows over the period of time with a compounding effect. The account maintenance charges being low, the benefit of accumulated pension wealth to the subscriber eventually become large.

- Ease of Access: The NPS account is manageable online. An NPS account can be opened through the eNPS portal. Further contributions can be also be made online through the following eNPS portals of CRAs: NSDL CRAKfintech CRA

- Once the PRAN account is opened, an online login id and password is provided to the subscriber. He/she can login and view/manage his NPS account online, over a click.

Why should I open NPS Account?

Opening NPS account has its own advantages as compared to other pension product available. Below are few features which make NPS different from others:

- Low cost product

- Tax breaks for Individuals, Employees and Employers

- Attractive market linked returns

- Easily portable

- Professionally managed by experienced Pension Funds

- Regulated by PFRDA, a regulator set up through an act of Parliament

Who manage my funds in NPS?

At present there are 8 Pension Funds (PFs) who manage the subscriber funds at the option of the subscriber. At present, Subscriber has option to select any one of the following eight pension funds:

• ICICI Prudential Pension Fund

• LIC Pension Fund Ltd

• Kotak Mahindra Pension Fund

• Reliance Capital Pension Fund

• SBI Pension Fund

• UTI Retirement Solutions Pension Fund

• HDFC Pension Management Company Ltd

• Birla Sunlife Pension Management Ltd.

However, this list may undergo changes if new pension fund managers are registered by PFRDA or existing players are de-registered by PFRDA.

What are the investment options available in NPS?

NPS offers you two approaches to invest in your account:

- Active choice

- Auto choice

In Active choice, Subscriber selects the allocation percentage in assets classes, however, in Auto choice, funds are automatically allocated amongst asset classes in a pre-defined matrix, based on the age of the subscriber. After selection of pension fund manager, Subscriber also has to exercise the choice of investment.

What is Active choice in NPS?

Active choice:

Unlike traditional investment products, NPS offers you with the flexibility to design your own portfolio. Depending on your risk appetite, you can design your portfolio by allocating Funds amongst available four asset classes. This is called Active Choice. Following are the four asset classes are available under Active choice:

- Equity or E

- Corporate Debt or C

- Government Securities or G

- Alternative Investment Funds or AIF

What is Auto choice in NPS?

Auto Choice:

At times designing your portfolio can be a little delicate and time consuming. NPS gives you the flexibility to opt for a dynamic and automatic allocation of your portfolio in case you do not want to exercise an Active choice. This option is called the Auto choice.

In Auto choice, your money will be invested in asset classes – E, C and G – in defined proportions based on your age.

As individual’s age increases, exposure to Equity and Corporate Debt is gradually reduced and that in Government Securities is increased. Depending upon the risk appetite of subscriber, there are three different options available within Auto Choice-Aggressive, Moderate and Conservative.

- Aggressive (LC-75) – Maximum Equity exposure is 75% up to the age of 35

- Moderate (LC-50) – Maximum Equity exposure is 50% up to the age of 35

- Conservative (LC – 25) – Maximum Equity exposure is 25% up to the age of 35

Where my money will get invested in NPS?

Following are the assets classes are available for investment under NPS:

- Equity or E- A ‘high return-high risk’ fund that invests predominantly in equity market instruments

- Corporate Debt or C – A ‘medium return-medium risk’ fund that invests predominantly in fixed income bearing instruments

- Government Securities or G – A ‘low return-low risk’ fund that invests purely in Government Securities

- Alternative Investment Funds or A –In this asset class, investments are being made in instruments like CMBS, MBS, REITS, AIFs, Invlts etc.

If you are a conservative investor, you can choose to invest your entire pension wealth in C or G asset class. However, if you want to have exposure to equity, you can allocate maximum 50% of your money to asset class ‘E’ or up to 5% in Alternative Investment Funds.

What is Tier I & Tier II account means in NPS?

NPS provides you two types of accounts: Tier I and Tier II. Tier I is mandatory retirement account, whereas Tier II is a voluntary saving Account associated with your PRAN.

Tier II offers greater flexibility in terms of withdrawal, unlike Tier I account, you can withdraw from your Tier II account at any point of time.

The following are the salient features of the Tier-I and Tier-II accounts:

Tier-I account: This is a restricted and conditional withdrawable retirement account which can be withdrawn only upon meeting the exit conditions prescribed under NPS.

Tier-II account: This is a voluntary savings facility available as an add-on to any Tier-1 account holder. Subscribers will be free to withdraw their savings from this account whenever they wish.

Below are few significant benefits of Tier II NPS Account:

- No additional annual maintenance Charge

- Saving for your day to day need (withdrawal at any point of time)

- Transfer fund to pension account ( Tier I) any time

- No minimum balance required

- No levy of exit load

- Separate Nomination facility available

- Option to select different Investment pattern from Tier I

Can I open a Tier II Account in NPS?

Subscriber who has an active Tier I account can activate a Tier II account

- It is open for any resident Indian, NRI can’t activate Tier II account.

- It can also be opened along with Tier I account.

- All Government Subscribers who are mandatorily covered under NPS and have active Tier I account, can activate Tier II account.

How and where can I open a NPS account?

For all citizens and corporates wishing to provide this facility to their employees, NPS is distributed through various authorized Points of Presence (POP’s) and currently almost all the banks (both private and public sector) are enrolled to act as Point of Presence (POP) apart from several other financial institutions.

To invest in NPS, you can open an account with a Point of Presence (POP) or online through eNPS platform.

You can open NPS account online through eNPS if you have following documents:

(I) Aadhaar Card, or

(ii) PAN card with Savings account in one of the empanelled bank undertaking KYC verification

online.

List of the empanelled bank is available on the eNPS platform available on NPS Trust website www.npstrust.org.in

What are the documents that need to be submitted for opening a NPS account?

The following documents need to be submitted to the POP for opening of a NPS account:

a. Completely filled in subscriber registration form

b. Proof of Identity

c. Proof of Address

d. Age/date of birth proof.

e. Cancelled Cheque (if applicable)

Is there any minimum annual contribution requirements under NPS?

Yes, A subscriber has to contribute a minimum annual contribution of Rs.1000/- for his/her Tier I account in a financial year and if not contributed the account will be frozen.

In order to reactivate the account, the customer has to pay the minimum contribution of Rs. 500/- .

In order to unfreeze an account the subscriber has to approach the Point of Presence (POP) and pay the required amount, or he/she can make contribution through eNPS platform.

The following table provides the complete information on the minimum contribution requirements:

What is the minimum contribution required under NPS?

A Subscriber is required to make initial contribution (minimum of Rs. 500 for Tier I and a minimum of Rs. 1000 for Tier II) at the time of registration.

Subsequently, a Subscriber can make contribution subject to the following conditions:

Tier I:

- Minimum amount per contribution – Rs. 500

- Minimum contribution per Financial Year – Rs. 1,000

- Minimum number of contributions in a Financial Year – one

Over and above the mandated limit of a minimum of one contribution in Tier I, a Subscriber may decide on the frequency of the contributions across the year as per his / her convenience.

Tier II:

- Minimum amount per contribution – Rs. 250

- No minimum balance required

How many nominees are allowed under NPS? Can a minor be a nominee?

Subscriber is allowed to register up to three nominees in NPS. Yes, minor can be a nominee. In such case, Subscriber will be required to provide guardian’s details and date of birth of the minor.

When I Can Close My NPS Account?

As per PFRDA (Exits & Withdrawals under NPS) Regulations 2015, in following conditions Subscriber can exit from NPS:

- Upon Superannuation – When a subscriber reaches the age of Superannuation/attaining 60 years of age, he or she will have to use at least 40% of accumulated pension corpus to purchase an annuity that would provide a regular monthly pension. The remaining funds can be withdrawn as lump sum.

If the total accumulated pension corpus is less than or equal to Rs. 2 lakh, Subscriber can opt for 100% lumpsum withdrawal. - Pre-mature Exit – In case of pre-mature exit (exit before attaining the age of superannuation/attaining 60 years of age) from NPS, at least 80% of the accumulated pension corpus of the Subscriber has to be utilized for purchase of an Annuity that would provide a regular monthly pension. The remaining funds can be withdrawn as lump sum. However, you can exit from NPS only after completion of 10 years.

If the total corpus is less than or equal to Rs. 1 lakh, Subscriber can opt for 100% lumpsum withdrawal. - Upon Death of Subscriber – The entire accumulated pension corpus (100%) would be paid to the nominee/legal heir of the subscriber.

What are Annuity Schemes available under NPS?

Following schemes are available with ASPs under NPS:

- Annuity for life– On death of the annuitant, payment of Annuity ceases.

- Annuity for life with return of purchase price on death– On death of the annuitant, payment of Annuity ceases and the purchase price is returned to the nominee

- Annuity payable for life with 100% Annuity payable to spouse on death of annuitant– On death of the annuitant, Annuity is paid to the spouse during life time. If the spouse predeceases the annuitant, payment of Annuity will cease after the death of the annuitant.

- Annuity payable for life with 100% Annuity payable to spouse on death of annuitant with return on purchase of Annuity– On death of the annuitant, Annuity is paid to the spouse during life time and purchase price is returned to the nominee after the death of the spouse.

What options for exit from NPS are available for Subscriber at the time of Superannuation/at the age of 60?

Subscriber can decide to remain invested in NPS (Up to 70 years) or can exit from NPS. Following options are available to NPS Subscribers:

- Continuation of NPS account:

Subscriber can continue to contribute to NPS account beyond the age of 60 years/superannuation (Up to 70 years). This contribution beyond 60 is also eligible for exclusive tax benefits under NPS. - Deferment (Annuity as well as Lump sum amount):

Subscriber can defer Withdrawal and stay invested in NPS up to 70 years of age. Subscriber can defer only lump sum Withdrawal, defer only Annuity or defer both lump sum as well as Annuity. - Start your Pension:

If Subscriber does not wish to continue/defer NPS account, he/she can exit from NPS. He/she can initiate exit request online and asper NPS exit guidelines start receiving pension.

Can I claim 100% Withdrawal in case of Superannuation and Pre-mature Exit?

Yes, a subscriber can claim withdrawal in following cases:

In case of Superannuation- A Subscriber can claim 100% Withdrawal if the total accumulated corpus is less than or equal to Rs. 2 Lakh at the time of Superannuation/attaining age of 60 years.

In case of Pre-mature Exit- If total accumulated corpus is less than or equal to Rs. 1 Lakh, the Subscriber can avail the option of complete Withdrawal. However, you can exit from NPS only after completion of 10 years.

Can I withdraw some amount during my tenure in NPS and still continue to subscriber to my NPS Account?

Yes, NPS Subscriber can withdraw certain amount out of his own contribution. It is considered as partial withdrawal under NPS.

Following are the conditions of Conditional Withdrawal:

- Subscriber should be in NPS atleast for 3 years

- Withdrawal amount will not exceed 25% of the contributions made by the Subscriber

- Withdrawal can happen maximum of three times during the entire tenure of subscription.

- Withdrawal is allowed only against the specified reasons, for example;

- Higher education of children

- Marriage of children

- For the purchase/construction of residential house (in specified conditions)

- For treatment of Critical illnesses

In case of pre-mature exit in NPS, when shall the pension starts?

What are the tax benefits under NPS?

Tax Benefit available to Individual:

Any individual who is Subscriber of NPS can claim tax benefit under Sec 80 CCD (1) with in the overall ceiling of Rs. 1.5 lac under Sec 80 CCE.

Exclusive Tax Benefit to all NPS Subscribers u/s 80CCD (1B)

An additional deduction for investment up to Rs. 50,000 in NPS (Tier I account) is available exclusively to NPS subscribers under subsection 80CCD (1B). This is over and above the deduction of Rs. 1.5 lakh available under section 80C of Income Tax Act. 1961.

Tax Benefits under the Corporate Sector:

- Corporate Subscriber:

Additional Tax Benefit is available to Subscribers under Corporate Sector, u/s 80CCD (2) of Income Tax Act. Employer’s NPS contribution (for the benefit of employee) up to 10% of salary (Basic + DA), is deductible from taxable income, without any monetary limit. - Corporates

Employer’s Contribution towards NPS up to 10% of salary (Basic + DA) can be deducted as ‘Business Expense’ from their Profit & Loss Account.

Please note: Tax benefits are applicable for investments in Tier I account only.

What are other tax benefits under NPS apart from available u/s 80CCD?

Apart from tax benefits available under 80CCD, below are the other tax benefits available under NPS:

- Tax benefits on partial withdrawal:

Subscriber can partially withdraw from NPS tier I account before the age of 60 for specified purposes. According to Budget 2017, amount withdrawn up to 25 per cent of Subscriber contribution is exempt from tax. - Tax benefit on Annuity purchase:

Amount invested in purchase of Annuity, is fully exempt from tax. However, annuity income that you receive in the subsequent years will be subject to income tax. - Tax benefit on lump sum withdrawal:

After Subscriber attain the age of 60, up to 40 percent of the total corpus withdrawn in lump sum is exempt from tax.

For example: If total corpus at the age of 60 is 10 lakhs, then 40% of the total corpus i.e. 4 lakhs, you can withdraw without paying any tax.

So, if you use 40% of NPS corpus for lump sum withdrawal and remaining 60% for annuity purchase at the time of retirement, you do not pay any tax at that time. Only the annuity income that you receive in the subsequent years will be subject to income tax.

What are the tax benefits on investments under Tier II account?

There is no tax benefit on investment towards Tier II NPS Account.

How Accurate is Moneycontain NPS Calculator?

At moneycontain I always make sure there is no room for error because it is about your money, therefore you see any calculator on the moneycontain is gone through a accuracy check from a prominent websites.

There are many calculator available online to calculate NPS returns, However you can only trust the numbers if it is from the official website i.e. NPStrust.org.in

Therefore I have made comparison of Moneycontain NPS Calculator to NPS official Calculator.

I have taken a screenshot from NPS calculator from NPS website and compared the results with same amount using moeycontain NPS Calculator. Checkout the images below to know the result.

As you can see I have entered the similar values, in moneycontain NPS Calculator and below is the result which matches exactly with the official NPS website calculator.

The only reason I do this on all financial calculator on moneycontain is to be on safer side as most calculator available online may show you wrong results.

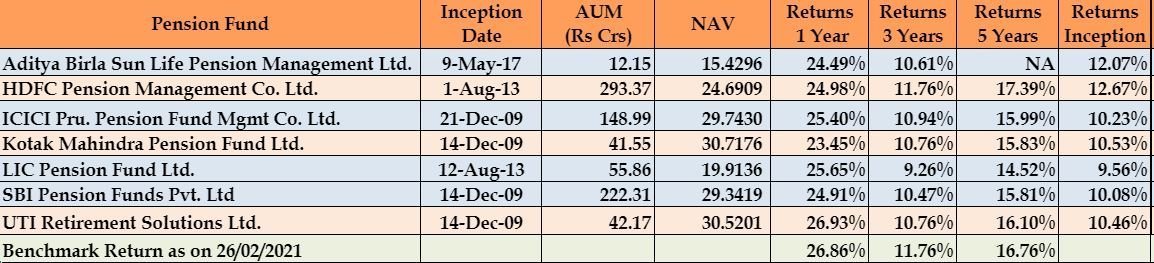

National Pension Scheme (NPS) Returns:

Let us checkout how much cagr return NPS has generated since inception under various fund managers and what is the returns NPS is giving in last 1, 3, 5 years range.

As we can see from the above data historical trends shows the average returns from NPS Scheme since inception is in range of 8 to 15% which is great. Moreover there are various other schemes to get the returns detail for each NPS Scheme you can check here.

Can I switch from one investment scheme to another in NPS?

Yes, NPS offers to its subscribers the option to change the scheme preference. Subscriber has option to realign his/her investment in asset class E, C G and A based on age and future income requirement.

Also, the subscriber has option to change the PF and the investment option (active/auto choice).

How the annuity OR monthly pension is paid IN NPS?

Monthly pension /Annuity in NPS will be paid through direct bank transfer to the specified subscribers bank account only.

Frequently Asked Question (FAQ):

Is NPS risk free?

No, NPS aka National Pension Scheme is a market linked scheme, the funds you deposit gets deposited in different financials instruments such as equity, debt, government bonds etc. hence NPS does poses a risk, Having said that if you look at the historical returns NPS has given more than 8 to 15% returns on average since inception.

Can I invest more than 50000 in NPS?

Yes, you can invest more than Rs.50,000 in a financial year or even a month there is no maximum/upper limit

What happens to NPS if I die after 60?

Incase the subscriber die the entire wealth accumulated (100%) through NPS will be given to the nominee of the account holder.

What is the lock in period for NPS?

The lock in period is upto 60 years of age since you open the NPS account, however there is a option of pre-mature withdrawal after 10 years also.

In case of pre-mature exit (exit before attaining the age of superannuation/attaining 60 years of age) from NPS, at least 80% of the accumulated pension corpus of the Subscriber has to be utilized for purchase of an Annuity that would provide a regular monthly pension.

The remaining funds can be withdrawn as lump sum. However, you can exit from NPS only after completion of 10 years. If the total corpus is less than or equal to Rs. 1 lakh, Subscriber can opt for 100% lumpsum withdrawal.

Can I have more than one NPS account?

No, multiple NPS accounts for a single individual are not allowed and there is no necessity also as the NPS is fully portable across sectors and locations.

Can NPS be withdrawn anytime?

Yes, NPS Subscriber can withdraw certain amount out of his own contribution. It is considered as partial withdrawal under NPS.

Following are the conditions of Conditional Withdrawal:

- Subscriber should be in NPS atleast for 3 years

- Withdrawal amount will not exceed 25% of the contributions made by the Subscriber

- Withdrawal can happen maximum of three times during the entire tenure of subscription.

- Withdrawal is allowed only against the specified reasons, for example;

- Higher education of children

- Marriage of children

- For the purchase/construction of residential house (in specified conditions)

- For treatment of Critical illnesses

Is it mandatory to deposit every year in NPS?

Yes, a subscriber is required to make initial contribution (minimum of Rs. 500 for Tier I and a minimum of Rs. 100 for Tier II) at the time of registration.

Subsequently, a Subscriber can make contribution subject to the following conditions:

Tier I:

- Minimum amount per contribution – Rs. 500

- Minimum contribution per Financial Year – Rs. 1,000

- Minimum number of contributions in a Financial Year – one

Over and above the mandated limit of a minimum of one contribution in Tier I, a Subscriber may decide on the frequency of the contributions across the year as per his / her convenience.

Tier II:

- Minimum amount per contribution – Rs. 250

- No minimum balance required

What is maximum limit for NPS?

There is no maximum limit or upper cap for investment in NPS in a financial year.

Is NPS better than PPF?

National Pension Scheme (NPS) is a market-linked pension scheme offered by the Government of India. Public Provident Fund (PPF) is a government-backed savings scheme.

Their similarity is that the government offers both. Having said that, Returns on NPS are market linked. They are around 8-15% p.a on average.

Whereas for PPF, returns are fixed and it is in the form of interest which ranges between 7.1 to 8.9 %p.a. NPS falls under moderate to high risk category, while PPF is a low risk investment.

Look at the below image to know more:

Can I pay NPS monthly?

Yes, you can make monthly contribution or even in a year in NPS. Higher the monthly contribution more is the pension wealth accumulated at the end.

Can I invest in both PPF and NPS?

Yes, you can make investment in Public Provident Fund as well as National Pension Scheme. They both are different financial products offered by the Government of India.

Which bank NPS is best?

There is no such thing as the best bank for NPS, you can open account with any bank who is offering you the NPS services. Keep in mind you can even select the fund type and fund manager after looking at the returns they have created over a period of time to be on the safer side.

Is Tier 2 NPS taxable?

Yes, tier 2 NPS is taxable, Tax benefits are applicable for investments in Tier I account only.

Conclusion:

NPS is a long term retirement savings scheme which builds up the pension wealth through effective investments of the subscriber contributions over the term of the subscriber’s continuation in the scheme.

NPS account can be operated from anywhere in the country irrespective of individual employment and location/geography.

Subscribers can shift from one sector to another like Private to Government or vice versa or All Citizen Model to Corporate Model and vice versa. Hence a private citizen can move to Central Government, State Government etc. with the same Account.

Also subscriber can shift within sector like from one POP to another POP and from one POP-SP to another POP-SP. Likewise an employee who leaves the employment to become a self-employed can continue with his/her individual contributions.

If he/she enters reemployment he/she may continue to contribute and his/her employer may also

contribute and so on.

These all features make National Pension Scheme a great investment option for everyone.

If, you have liked the content please do share it with your friends or on social media, as sharing do bring the good karma. If you have any questions or feedback you can leave them in comment box below.

ELSS Calculator For Monthly SIP And Lumpsum SIP- Calculate Returns In 3 Quick Step

Incase you are looking for any Home loan or want to calculate the monthly EMI, than do check moneycontain free home loan EMI calculator.

Note: Please do not take this as any recommendation, to trade or invest. This is just for reference, to make you understand more about NPS Calculator and its importance, under no circumstances intended to be used or considered as financial or investment advice, a recommendation or an offer to sell, or a solicitation of any offer to buy any securities or other form of financial asset.

Please do your own research and make investment. Moneycontain will not be responsible for any of your losses at all. The point made is for educational purpose only. All investments are subject to risks, which should be considered prior to making any investments.

{kind=link}