Use below Moneycontain ELSS Calculator to find out how much you can expect as a return when you make a monthly SIP or lumpsum (one time) SIP in ELSS Funds. Equity Linked Saving Schemes (ELSS) is one of the best tax saving mutual funds scheme at present in India.

You will be surprised to know that ELSS is the only mutual fund which qualifies for a tax deduction of up to Rs. 1.5 lakh annually under Section 80C of the Income Tax Act.

Most importantly this a three in one ELSS calculator which means now you can calculate monthly SIP return or Lump Sum investment in SIP or both monthly as well as Lump Sum return at once.

You just need to enter the monthly or Lumpsum amount invested, enter expected return (usually over and above 12%p.a.), enter investment period (in months) make sure it should be minimum 3 years as ELSS have a 3 year lock-in period, it will give you the future value as well as tells you about the wealth gained on investment made.

Moneycontain ELSS Funds Returns Calculator helps you to concentrate on your financial planning through ready to use ELSS Calculator, It will reveal how much your net worth would be down the line, taking into consideration the various variables including the type of investment like SIP or Lumpsum along with the investment duration and expected rate of return.

So, go ahead and check how much you will get if you make investments in Equity Linked Saving Schemes (ELSS) on maturity.

Now, that you have calculated the returns from ELSS funds, its time to deep dive in to some facts about ELSS and how it works? step by step.

What Is ELSS (Equity Linked Saving Schemes)?

Equity Linked Saving Schemes (ELSS), is widely known as tax saving mutual funds, basically ELSS are equity oriented mutual funds. As the as major part of the assets are allocated to equities, a part of the corpus is also invested in debt instruments.

As per the SEBI regulations, ELSS funds have to invest at least 80% of their corpus in equity or equity related instruments.

ELSS falls under the category of ‘High Risk with High Returns’. These funds come with a lock in period of 3 years and qualify for tax deduction under Section 80C.

Investments in ELSS of up to Rs 1.5 lakh per financial year can be claimed as tax deduction under this Section. These schemes are also sponsored by the Government of India (GOI) to promote a habit of long-term investment among masses.

One can make a investment in ELSS funds either through systematic investment plan (SIP) every month or even through a lumpsum (one time) investment with as low as Rs.500.

ELSS is an open-ended Equity Mutual Fund that not only is great for tax saving purposes but also creates a growth opportunity for your investment.

An open-ended fund allows investors to enter and exit the fund anytime after the NFO, whereas a close-ended fund restricts the entry and exit of investors to the NFO period.

NFO stands for New Fund Offer. When a mutual fund scheme offers its units for the first time for investments, it is known as a New Fund Offer (NFO). In its essence, a New Fund Offer is similar to an Initial Public Offering (IPO).

Another thing is, unlike close ended funds, open ended funds do not have a limitation on the number of units they can issue. More units of an open ended fund get created when an investor invests money in the fund.

Likewise, when an investor redeems units of an open ended fund, the mutual fund units are taken out of circulation.

While open ended funds allow investors to make use of systematic plans – systematic investment plans (SIPs), close ended funds do not support this facility.

I hop you now have a basic understanding of what exactly is ELSS Funds? before we move on to understand other significant information let us make a quick accuracy check of ELSS calculator.

How Accurate Is Moneycontain ELSS Calculator?

Moneycontain ELSS calculator helps you calculate estimated returns on the capital invested. When we talk about investments, the most important aspect is what kind of returns can be expected.

Returns can be quite varied in nature over a long period of time. Hence, it would be difficult to figure out what the eventual corpus would be at different expected rate of returns.

At moneycontain I always make sure there is no room for error because it is about your money, therefore you see any calculator on the moneycontain is gone through a accuracy check from a prominent banking websites.

Therefore I have made comparison of Moneycontain ELSS Calculator to SBI ELSS Calculator.

I have taken a screenshot from SBI ELSS calculator and compared the results with same amount using Moneycontain ELSS Calculator. Checkout the images below to know the result.

As you can see the result are accurate to SBI for Lumpsum SIP in ELSS Funds , now let us see the results for SBI and Moneycontain for Monthly SIP in ELSS Funds below:

As you saw in above comparison of ELSS Calculator for monthly as well as lumpsum, the results are as accurate as SBI Banking website.

The only reason I do this on all financial calculator on moneycontain is to be on safer side as most calculator available online may show you wrong results.

Let us move on to understand the major benefits of investing your money in ELSS Funds.

Why You Should Invest In ELSS Funds?

Below are the list of major benefits you as an investor in ELSS Funds can get:

Let us compare the tax benefits you stand to gain under different income brackets by investing in Equity Linked Savings Schemes (ELSS). Checkout the below image in order to understand the Tax Benefits of Equity Linked Savings Schemes (ELSS).

Why Not To Invest In ELSS Funds?

There are two disadvantage that I find while choosing to invest in ELSS Funds:

First is the Long Term Capital Gain Tax also known as LTCG Tax, (Since 31 January 2018 ) this gets charges upto 10% if the interest earned is more than rupees 1 lakh in a financial year without any indexation benefit. Indexation refers to the process that computes the cost of the asset factoring in the inflationary price rises.

Long-term capital gains tax is levied on the capital gains from shares and equity-oriented mutual funds, that are held for one year or more.

Having said that, your annual income should also comes in range of current tax slab in India and even if it comes there are many tax exemption benefits you can take to avoid taxes in legal manner.

How To Calculate LTCG On ELSS?

Suppose you invested Rs.3 lakhs in ELSS funds and after 3 years of lock-in period, the corpus that gets created is Rs.5 lakhs, now the interest earned from this investment is Rs.2 lakhs which means, Rs.1 lakh can be covered under exemption and the 10% LTCG will be charged on remaining Rs.1 Lakh. 10% of 1 lakh is Rs.10,000.

This is the amount which will get deducted under LTCG TAX, having said that under Section 54F one can save LTCG deduction.

Moreover, An Investment upto 1.5 Lakhs in Equity Linked Savings Scheme (ELSS) qualifies for income tax exemption under Section 80C of the Income Tax Act, 1961.

This means that your taxable income reduces by the amount of investment you make in ELSS. The amount of tax you pay gets reduced as your overall taxable income has now reduced

The second drawback is the Risk associated with investment in ELSS Funds. As you know it is a equity oriented scheme, so your money gets investment in equities which itself is counted under high risk category.

Therefore, the expectation of good CAGR returns is depended on stock market, which is in no way guaranteed like other government backed schemes such as Public Provident Fund (PPF).

So make your investment carefully and never make all investments in any one scheme at any time. Be diversified while doing investments of your hard earned money.

Let us now move on to know the list of best ELSS Funds in India in 2024 with great returns.

Which Are The Best ELSS Funds In 2024?

Investments in ELSS can give you higher returns like equity while saving tax too. Although, past performances are no guarantee to the returns in the future, they do however help by showing how the fund held up during adverse market conditions.

Checkout the top performing ELSS Funds in 2024 in below image with last 3 and 5 years returns comparison.

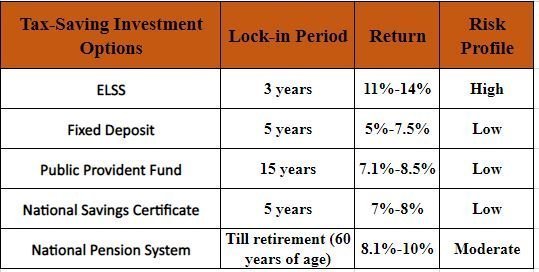

ELSS V/S FD/PPF/NSC/NPS Comparison:

ELSS funds don’t have guaranteed returns because they earn from investments in the equity market. However, the best performing funds have displayed the capability of generating inflation beating returns over the long-term.

This is something that fixed income tax saving investments like PPF, FD, NSC,NPS etc. tax saving instruments cannot do.

Checkout the below image to get a comparison between them:

How Much To invest in ELSS?

It depends on your financial goals, how much time you can give for investment as keeping in mind 3 year lock-in period, as well as your tax slab as an individual. There is no upper limit to make a investment in ELSS and the minimum is Rs.500.

However, the tax exempted amount is only Rs. 1.5 lakh in the financial year. One can also start with SIP or lump sum investment in ELSS. On a cautionary note make sure not to invest all money in any single scheme ever.

How To Start Investing in ELSS Funds?

Staring a investment in ELSS is as easy as making a online payment, thanks to dedicated online stock brokers such as Dhan, Zerodha, Upstox, Fyers, which allows its users to make a investment using their platform online and the best part is they all offer a direct plan instead of a regular plans.

With regular plans the returns will be lowered as extra commission apart from the expense ratio will be charged therefore it is advisable to invest using direct plans. One can even create a login account in any Asset Management Company (AMC) and start investing directly.

Why Invest In ELSS Funds?

The answer to this question is very simple, to beat Inflation. Due to inflation, the value of money decreases over time. For example if you have kept Rs. 1,00,000 with you as idle for 5 years instead of investing, assuming an inflation rate of 7% per annum the value of your money will be reduced to Rs.71,299 in percentage terms its -28.70% decline overall.

This is also known as discounting which factors in the rate of inflation impact on the future value of money in present terms. Hence one should know how inflation wipeout the large part of your saved money as well as investments.

Check out the below image to understand how inflation make a great impact even on your investments across different financial instruments such as Stock market (Equity), Mutual funds, FD, RD, Commodity & even real estate.

One need to understand “time value of money” as money loses its value over time, investing becomes important. Investing make sure a sustainable economic growth of a country and overall.

Therefore as an normal person or an investor you should know the (TMV) “time value of money” the value of money does not remain the same across time.

Meaning, the value of Rs.10000 today is not really Rs.10000 3 years from now. Oppositely, the value of Rs.10000 3 years from now is not really Rs.10000 as of today.

Whenever there is motion of time, there is an element of opportunity. Money has to be accounted or adjusted for that opportunity as in case inflation is that element.

Therefore it is very much important for you to make investments in mutual funds schemes such as ELSS Funds.

ELSS is also more transparent because it allows retrieving information related to investment, portfolio construction and past performance data as well.

What Is The ELSS Calculation Formula?

Although, using manual calculation for a ELSS return can be a daunting task, it is good to know in case one want’s. The ELSS returns are based on two primary methods, first is the monthly SIP calculation and second is the Lumpsum calculation.

The formula to calculate monthly SIP is :

FV = P × ({[1 + i]^n – 1} / i) × (1 + i)

In the above formula –

- FV (future value) is the amount you receive at the end of fund (maturity).

- P is the amount you invest at regular monthly intervals.

- n is the number of payments you have made(installments).

- i is the periodic rate of interest.

As I have already told you the formula looks very mumbo jumbo, specially for a person not from math’s or finance background.

The lumpsum sip calculation formula is:

A = P (1 + r/n) ^ nt

In the above lumpsum sip calculation formula:

A= Total Amount Receivable (at the end)

P= Total Amount Invested (initially)

R= Rate of Interest

T= Time (invested period)

N= No. of times the compound interest you receive in a year(yearly, half-yearly, quarterly, monthly)

Whenever you want to calculate your mutual fund return for lump sum SIP’s you can use this formula. Having said that, instead you can use Moneycontain ELSS Calculator online and get the returns quickly.

Let’s checkout some of the frequently asked question based on ELSS.

Frequently Asked Questions (FAQ):

How To calculate tax on ELSS?

LTCG Tax, (Since 31 January 2018 ) this gets charges upto 10% if the interest earned is more than rupees 1 lakh in a financial year, It is levied on the capital gains from shares and equity-oriented mutual funds, that are held for one year or more.

So, Suppose you invested Rs.2 lakhs in ELSS funds and after 3 years of lock-in period, the corpus that gets created is Rs.3.50 lakhs, now the interest earned from this investment is Rs.1.50 lakhs which means, Rs.1 lakh can be covered under exemption and the 10% LTCG will be charged on remaining Rs.50,000. 10% of 50K is Rs.5000.

This is the amount which will get deducted under LTCG TAX, having said that under Section 54F one can save LTCG deduction.

Is ELSS taxable after 3 years?

Yes, ELSS are taxable under Long term capital gain tax (LTCG), 10% LTCG tax is levied if the interest earned is more than rupees 1 lakh in a financial year.

How much tax can be saved by ELSS?

Under section 80C of Income Tax, one can avail tax benefit of upto ₹46,800 by investing upto ₹1.5 lakhs per year in ELSS. You can also invest more than ₹1.5 lakhs in ELSS, but tax benefit can not be availed on the investment exceeding ₹1.5 lacs per annum.

How do I redeem my ELSS after 3 years?

Upon maturity of your ELSS fund, you can simply opt out from the scheme and the money gets credited to your linked bank account. One can even make a transfer of funds, moreover you can also invest the same amount again to reap the maximum benefit of power of compounding.

ELSS will come under which section of Income Tax?

ELSS comes under Section 80C of the Income Tax Act, 1961.

Which is better ELSS or PPF?

If you are concerned about the rate of returns (ROI%) ELSS is much better than PPF, Having said that PPF is backed by Government of India with guaranteed returns and are not subject to market influence. PPF comes under Low Risk Profile whereas ELSS is a High Risk instrument.

PPF is mostly used for very long term investment period as it have a lock in period of 15 years on the other hand ELSS have a lock in period of just 3 years.

Can ELSS be Stopped Or Cancelled ?

Yes, you can cancel the ELSS by either filling a form offline and submitting to the AMC you have account with, or else online you can simply do this by cancelling the ongoing SIP in a click.

Can I Withdraw ELSS Funds Before 3 Years?

The simple answer to this question is No. ELSS investments do not provide the option to withdraw the investment amount before the end of the 3-year lock-in period. In ELSS, investors are given fund units against their invested amount. It is to these units that the lock-in period applies.

Is ELSS risk free?

ELSS investment portfolios are managed by trained and qualified fund managers who put in every bit of effort to protect the investors money and ensure high returns. Having said that, the risk is always associated as it is a market linked scheme.

Which is better monthly SIP or Lumpsum in ELSS?

Monthly SIP is better because of the “Rupee Cost Averaging factor”. Rupee Cost Averaging allows an investor to take advantage of the stock market volatility.

Through investing in a SIP, as an investor you will get more units when the Net Asset Value (NAV) is less and less units when the NAV is high. Which brings down the average cost of the all units over the long term investment.

Having said that Lumpsum SIP has its own advantage if you are buying it at the right time in right fund and when the Net Asset Value (NAV) is less which means you will have more units at a particular price and in long duration the NAV will be higher creating a bigger profit.

Other things with lump sum SIP is, there is no headache for every month keeping certain money in your account to maintain the SIP.

Can I Open ELSS without demat account?

Yes, there is no need to open a demat account to apply for ELSS.

What Is expense ratio in ELSS?

Expense ratio depicts how much of your investment goes towards managing the fund. A lower expense ratio translates into higher take-home returns. You need to choose that fund, which has a lower expense ratio.

Conclusion:

Investment in ELSS mutual is like “Killing two birds with one stone”. It not only serves as a tax saving option but also as a fantastic investment tool for wealth creation in the long term.

What makes it apart from other tax-saving options is its short lock-in period which is a minimum of 3 years.

ELSS also gives you the flexibility of choosing a diverse investment portfolio, including large-cap, mid-cap, small-cap, and others. Hence it is as of now one of the best investing option available to you in India.

If, you have liked the content please do share it with your friends or on social media, as sharing do bring the good karma. If you have any questions or feedback you can leave them in comment box below.

Note: Please do not take this as any recommendation, to trade or invest. This is just for reference, to make you understand more about ELSS Calculator and its importance, under no circumstances intended to be used or considered as financial or investment advice, a recommendation or an offer to sell, or a solicitation of any offer to buy any securities or other form of financial asset.

Please do your own research and make investment. Moneycontain will not be responsible for any of your losses at all. The point made is for educational purpose only. All investments are subject to risks, which should be considered prior to making any investments.

{kind=link}